There is no such thing as a purely capitalist economy and like many, Zimbabwe is a mixed economy. However, we have flirted with socialism more than most with our ‘command’ efforts in recent times as an example.

We still have a somewhat limited free market though. Although the government loves to exert control in the economy, it is in spite of their price controls for example that the economy trudges along. One of the reasons it crawls along rather than sprint is the shortage of ‘oil’ that a capitalist economy runs on – credit.

I’m not a fan of the credit lifestyle but I have to admit it’s a quick way to lubricate the cogs of capitalism. Credit allows people to buy or build houses just as well as it entices them to splurge on unessential stuff that they can’t afford.

When people are offered goods on credit they (we) really do feel like we got it for free for a second. You might see an item you like going for say $300 and you might really want it but having to fork out $300 outright might force you to postpone the purchase. However, if the trader said you could pay $15 a month for it until you’re done, then the decision is pretty much made for you. You take the deal and business thrives.

That’s not to mention the business ideas confined to business plans stored in rarely opened files on a computer somewhere. We all know about how Nigel Chanakira put up his parents’ house as collateral to get a loan to start Kingdom Bank. Without that loan, who knows if Kingdom would have ever been.

We had a taste of credit in Zimbabwe

Our parents, as young couples, bought most of their furniture on credit from places like Nyore Nyore and Pelhams. They got clothes for their kids at Edgars/Truworths and that little Edgars magazine was part of our reading growing up.

Even some of the working class, not to mention the middle class were lucky enough to get mortgages on little houses that needed extending. This all worked on credit.

Then hyperinflation happened and loan repayments were impossible to keep up with as interest rates soared. Houses were repossessed, lenders had to write off substantial losses and the public lost faith in the system.

A creditless Zimbabwe born

Zimbabwe emerged as a shadow of itself after the hyperinflation era. One of the reasons the economy has struggled to lift off is that the oil of capitalism has been missing – there is no credit.

Entrepreneurs are struggling to grow their businesses for lack of funding. The general population is living hand to mouth and has no appetite for ‘luxuries’ that require outright cash outlays. ‘Luxuries’ in the Zimbabwean context now referring to all that is not food or shelter.

That means business will struggle. It makes sense though for businesses to offer their products/services on credit/layby. Like I mentioned earlier, people are more likely to buy even what they don’t need when there are good payment plans.

It is no secret that a lot of people run a pirated version of Windows. When you find that you need $199 for Windows 10 Home you get why that is. That often is how much the laptop itself would have cost on the second hand market. Imagine though if there was a 3 year credit facility and one could pay $6 a month. That could sway some to go legit.

Why is there no credit?

Borrowers fear interest rate hikes

We touched on it and trust, or the lack thereof is a major factor. The general population fears interest rate hikes that can make repayments impossible. So, while we get why the RBZ increased interest rates recently from 60% to 80% we also know that that scares borrowers.

We do note that the inflation rate is right up there with the interest rate and so in real terms the 80% interest rate is reasonable. As reasonable as paying $80 interest on a $100 loan can be. However, USD loans provide a way to get around that messiness.

When both lender and loanee do not have to worry about a fast depreciating currency, they can agree on a more palatable interest rate. We find that in the market, one can get a USD loan on good terms.

Lenders fear defaults

When it comes to lenders, it is mostly those in the financial sector that can offer lending. That is because of the inherent risks in lending someone money, they may fail to pay you back. So, financial institutions being the ones that maintain people’s bank accounts are in a better position to know how risky each individual is.

So, why have financial institutions been reluctant to lend out? We touched on it. Our rollercoaster economy, high inflation and currency challenges increase risk of default.

Lack of cooperation

Then there is the lack of cooperation between financial institutions. Even the RBZ governor is on record decrying the lack of cooperation between his subjects. So, it then means there is no way for a bank to know how risky a certain individual is.

They say once bitten, twice shy. Banks were duped by individuals who took out loans at various banks and then defaulted. The lack of cooperation meant the banks had no idea just how much debt a loan applicant had at other banks. So, they ended up lending to high profile individuals who were already up to their necks in debt.

The major defaults that followed shook the industry and ended with a special vehicle being created by the government (Zamco) to take over some of those loans.

The lesson was learnt and banks just decided it wasn’t worth it to lend out. They were not willing (able?) to work together to fix the information sharing problem and drastically decided to just cut everyone off.

The RBZ’s credit registry

“In an endeavour to promote access to credit by individuals, the corporate sector as well as small to medium enterprises, the Reserve Bank of Zimbabwe and the government have taken measures to enhance the credit infrastructure in the country through the establishment of a central credit registry.”

That’s literally the first paragraph on the introduction of the central credit registry. The RBZ decided to step in and collect and share information on individual borrowers and business’ borrowing habits and repayment patterns.

After collecting that information, the registry comes up with a credit score for the person. I asked for my own report and I couldn’t be rated because I have never taken a loan from any financial institution hence no borrowing habits or repayment patterns. That means I am a black box to any would-be lender, making them reluctant to lend to me. One of them will have to take a risk on me.

The central registry does not blacklist anyone or advise any lender on who to lend to. The lender is free to ignore a terrible or nil credit score.

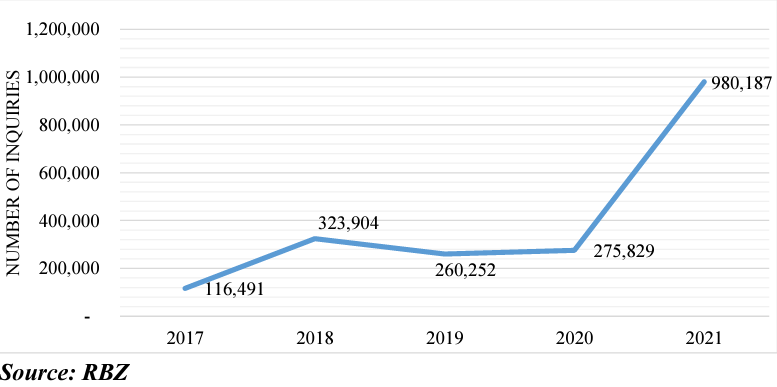

The registry did not have the most explosive of starts but it does appear as if it’s starting to pick up steam.

Trend of Inquiries at the credit registry shows inquiries rising from; 116491 in 2017, 323904 in 2018, 260252 in 2019, 275829 in 2020 and a massive jump to 980187 in 2021.

Most of those inquiries represent a would-be lender checking to see if a would-be borrower is low risk. That’s encouraging to see because no lender would go through all that if they were not seriously considering lending to someone. 2021 stats show that that’s the case.

Zimbabwean lenders are stepping up

In the Monetary Policy for 2022 we found out that “the number of active clients accessing loans through microfinance institutions increased by 10.66% from 288 561 as at 31 December 2020, to 307 673 as at 31 December 2021.”

The number of persons getting loans may have only increased by 10.66% but the value of the loans grew by 262.69% from ZW$2.01 billion as at 31 December 2020, to ZW$7.29 billion as at 31 December 2021. That’s something, considering year on year inflation was ‘only’ 61% that December 2021.

Banks joined in on the fun and loosed their purse strings too. Total loans and advances grew 179%, from ZWL$82.4 billion in 2020 to ZWL$229.9 billion in 2021.

Don’t get it wrong though, they are still cautious. The loan to deposit ratio grew from 39.45% to 48.27% against a benchmark of 70%. Personally, I’m not even comfortable with banks lending out almost half of all our deposits so would accept the 48.27% ratio.

However, if we’re committed to this capitalist dream we need them to bump that up closer to 70% and stimulate activity in the economy.

To note is that of that ZWL$229.9 billion in loans, 36.8% were foreign currency denominated.

There’s still a problem though

I mentioned that I do not have a credit score and if you’re like me, your chances of getting a loan are low. I also do not have good collateral, further decreasing my chances. Then there is the little issue of not being a civil servant which means I might as well not even try.

See, most loans in the market are salary based. Unfortunately, not all salaries are the same. Everyone trusts that someone employed by the government will get their salary and that arrangements to deduct repayments from that salary are not difficult to initiate.

So, a private company has to negotiate with lenders and assure them that an individual will be in their employ for the foreseeable future and that they can arrange to deduct loan repayments straight from payroll.

This means an individual employed by a small to medium private company has to convince their employer to negotiate with a lender and sign memorandums of agreement before they can dream of getting a loan. Needless to say, for most people that is not going to happen.

This caution by lenders is understandable and its results are clear to see. The international benchmark for the non performing loans to total loans ratio is 5%. Lenders are okay with 5% of loanees defaulting. The actual rate in Zimbabwe in 2021 was 0.94%.

You just have to commend the lenders here. They increased their loans but still managed to maintain a default rate that low. That’s some impressive risk management right there.

That problem though

Most Zimbabweans are not formally employed and neither do they have good collateral. Being cut off from the official financial markets they also do not have a record of their borrowing and repayment habits. There will be no loans for these people.

It can be frustrating sometimes to realise that it’s mostly those individuals who already have houses that can get mortgages to buy new houses. The fresh faces leaving college and entering the job market are in for a rude awakening. Those who like Winky D thought they would have their own houses by 25 will learn the lesson.

This means the same individuals that got loans in the past will get loans. That’s how it works. We saw how the number of active clients for microfinance institutions only increased by 10.66% in 2021.

In trying to cater to even the risky borrowers, some of these lenders are straight up turning into loan sharks.

Do you even want that credit?

The interest rate determines if a loan is a good deal. The interest has to compensate the lender for taking the risk whilst reasonable for the borrower too. Some of the microfinance institutions I visited are straight up thugs.

The worst I heard was that I would have to give up a car as collateral and have it parked in some garage for as long the loan has not been fully repaid. I thought, fair enough, you really would be taking a chance on me and for all you know I might disappear as soon as you give me the money. The car thing was reasonable to me to be honest.

Then came the interest rate and I almost fainted – 30% per month. You read that right, 30% per month, not per year. In only 4 months the interest paid on the loan would be more than the principal. You have to have a very serious emergency to accept such loan terms. However, if you’re not going to get a salary based loan, expect such kinds of loan terms.

It’s not that much better for you if you have a payslip they can trust. Expect interest rates in the 25 – 30% range though this time it would be per annum and not per month.

That’s still pretty high for a foreign currency denominated loan. Do note that in many places you won’t even get the option for a Zimdollar loan, which makes sense to be honest.

Civil servants do not have to put up with such crazy interest rates as they can easily get 12% at some lenders that only serve government employees.

It all feels like the wild west

It’s good to see that lenders are slowly finding ways to inject money back into the economy. It is natural that after being burnt in the near past, they are doing this cautiously. They feel it’s still risky and so are turning away most and in some cases are demanding limbs for their loans.

The only problem is that the startup looking to get off the ground does not qualify for the loans with reasonable interest rates. Leaving them with only the loan sharks.

What kind of growth would a company expect to justify getting a loan with 30% interest per month? If an entrepreneur took that loan I would be less confident in their decision making. Whilst it’s good that such loans exist it still shows that we are still in the wild years and are putting up with exploitative practices just so we can get the ball rolling.

So, who is getting the loans and is that money going into productive use? I can guarantee you that the kid with a good idea and business plan working from their bedroom in their mother’s house is not getting any reasonable loan.

It’s okay, the world over banks and other financial institutions are not in the habit of lending to startups in their infancy. That’s the role venture capitalists and angel investors take. So, even if the loans are not going to startups and small businesses, they are increasing the buying power of individuals who then spend, increasing business for some company somewhere. I’m here for it.

The curious case of telcos discontinuing credit plans

You may remember when all 3 mobile network operators, Econet, NetOne and Telecel offered smartphone financing. This model is working wonders in more developed countries and credit ratings help companies decide who qualifies for such financing. In Zimbabwe, Econet said,

Currently, we do not offer any devices on credit or layby

The fact that they these plans were discontinued in Zimbabwe means one of two things. It’s either there was low uptake or there were high default rates. Now that the credit registry seems to be improving, we shall see whether those plans come back.

I would imagine there is an appetite for such financing. Right now I’m not in the least bit interested in shelling out $800 for a Galaxy S22 but if you offered me $33 a month I would be tempted. The comments we got when we talked about Apple looking to offer iPhones as subscription services show that Zimbos are not opposed to monthly installments for some of these expensive gadgets.-techzim